The seed cap-table veto that VCs never mention.

he seed terms a founder signs to survive the year are the same terms that quietly veto the round he needs two years later. Nobody reads them out loud until it is too late to change them.

A founder showed me his cap table last month. He showed it to me the way people show you a photograph of something they are proud of, turning the laptop around with a small flourish, waiting for me to be impressed. He had closed a seed round most of his peers would have envied. The money had come fast, from people in his own city who already knew the sector, and it had landed at a moment when the company badly needed it. To him that table was a foundation. It was proof the hard part was behind him.

I read it twice before I said anything, because I wanted to be sure I was reading it correctly, and because I already knew the next ten minutes were going to be unpleasant for both of us.

The money had not come from venture investors. It had come from a regional food distributor and two local property developers. Between them they held a controlling slice of the company. Each of them held an individual veto over any future issuance of equity. The distributor had been granted exclusive rights to sell the product in the home market. And to release the last tranche, the founder had pledged the company’s core intellectual property, the patents the entire business was built on, as collateral against a facility loan.

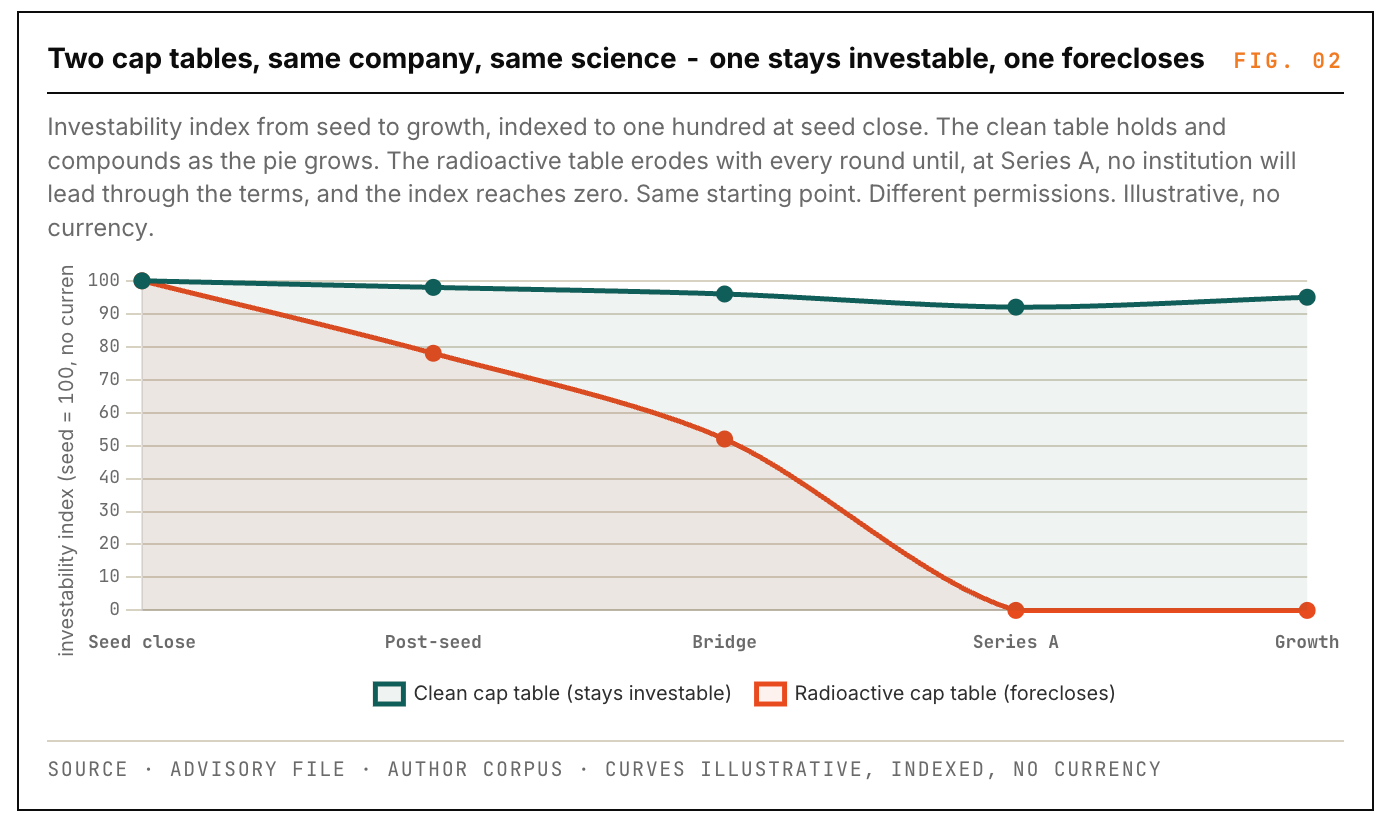

He thought he had raised a seed round. What he had actually done was sign a set of permissions that handed three people without venture experience the power to decide whether his company ever raised another euro. His cap table was not a foundation. It was structurally radioactive, and no tier-one institutional fund in Europe was going to lead his Series A while it stayed that way. I had to tell him that, slowly, while he was still holding the laptop turned toward me.

He is not unusual. He is the median. I see some version of this table more often than I see a clean one, and the founders attached to it are almost always serious, capable people who did the thing that felt responsible at the time. That is what makes this particular failure mode worth a whole issue. It does not happen to careless founders. It happens to careful ones who were told, correctly, that running out of cash kills companies, and who were never told that the cure can kill them more quietly than the disease.

The Myth.

The myth is that money is money. Take it where you can get it, keep the valuation up, and clean the rest up later.

It is the most pragmatic-sounding sentence in early-stage fundraising, and it is the one that ends the most companies that did not need to end. It treats capital as a commodity, interchangeable by the euro, distinguished only by how much of it you get and at what headline number. Under that belief the founder optimises for the two things he can see, the size of the cheque and the valuation printed on it, and barely reads the things he cannot yet feel, the control terms buried three pages into the agreement that decide who actually governs the company from that day forward.

The trouble is that seed capital is not a commodity. Two cheques of identical size, at an identical valuation, can carry terms so different that one builds a company and the other quietly forecloses on it. The euro is the same. The permissions attached to it are not. And the permissions are the part that compounds, because the next investor does not buy your valuation.

The next investor buys your cap table, your governance, and the question of whether the people already inside the company will let a new institution in on terms an institution can accept. Valuation is the headline. The terms are the company. Professional investors read the terms first, and most founders write them last.

The two ways the trap closes

The trap has two jaws. Founders usually walk into both at once, because they come from the same instinct, which is to treat the seed round as a problem of getting enough cash rather than a problem of getting the right cash.

The first jaw is control. A founder raising his first real money often takes it from whoever is closest and most willing, which in Food Biotech frequently means people outside venture altogether. A local corporate that wants a strategic foothold. A property developer with money to place and no idea what a liquidation preference does to a founder. A family office that knows the founder’s family. These investors are not villains. But they are unsophisticated in the specific sense that matters here, and unsophisticated capital asks for control as a substitute for the judgement it does not have. It cannot price the risk, so it demands to govern it. Board seats. Individual veto rights over future rounds. Commercial exclusivity. A blocking right on any valuation below some number. Each of these feels, in the moment, like a reasonable ask from someone writing a frightening cheque. Each of them is a permission you are giving away that the next investor will need back, and may not be able to retrieve.

The second jaw is capital intensity. Seed cash in a Food Biotech company is under constant pressure to become steel. There is always a custom fermenter to buy, a pilot skid to commission, a filtration line that would, the team insists, finally let them control their own process. Owned equipment feels like seriousness. It photographs well for the grant report and the investor update. And in most cases it is the single fastest way to convert irreplaceable seed runway into a depreciating asset that the next investor will value at close to nothing. Steel loses most of its worth the day it is installed and customised to your process. A stabilised yield, a regulatory dossier moving through its stages, a buyer who has paid you real money for real product: those appreciate. Seed capital spent buying capacity you could have rented is seed capital spent on the one category of thing that goes down in value while your runway goes down with it.

Both jaws close on the same hinge. The founder optimised for the visible thing, the cheque and the valuation and the owned plant, and mortgaged the invisible things, the governance and the cash and the freedom to raise again, that turned out to be the whole game.

The one move to make before Friday

Here is the move, and it is free, and you can run it this week whether you are about to sign a term sheet or you signed one a year ago and have been trying not to think about it.

Take your cap table and your current term sheet, real or proposed, and ask one question of every line in it: would a tier-one institutional fund agree to lead my next round with this term in place? Not tolerate it. Lead with it.

Go clause by clause. The individual veto over future issuance: would a lead investor accept a non-venture shareholder holding a unilateral block on the round they are trying to assemble?

The IP pledged as collateral: would a fund underwrite a company whose only real asset can be seized by a lender if a facility payment slips?

The exclusive distribution granted to a strategic: would a new investor fund a company that has already given away its home market for a seed cheque?

The owned plant bought with seed money: would a lead value it at what you paid, or at scrap?

For each line, the honest answer is yes, maybe, or no. Every no is a veto you have already signed against your own future round. You are not finding out whether your terms are friendly. You are finding out, while it is still cheap, which of your own clauses will cause an institution to pass before they have even looked at your science.

Most founders who run this honestly for the first time discover that the cap table they were proud of contains at least one hard no, and usually more. That discovery is uncomfortable and survivable if you make it yourself this quarter, while there is still time to renegotiate from a position of relative strength. It is close to fatal if a lead investor makes it for you in diligence eighteen months from now, because by then it is not a clause you can fix. It is the reason they passed, and they will rarely tell you it was the reason. They will simply stop replying, and you will think your science was not good enough, when in fact your governance was not investable.

This is Issue 33 of FoodEdge. The four radioactive clauses with the mechanism that makes each one lethal, the stage-adapted version of the question from pre-seed to growth, and the worked example are below for paid subscribers.